Apifiny Algo

Sophisticated API trading without the need for code!

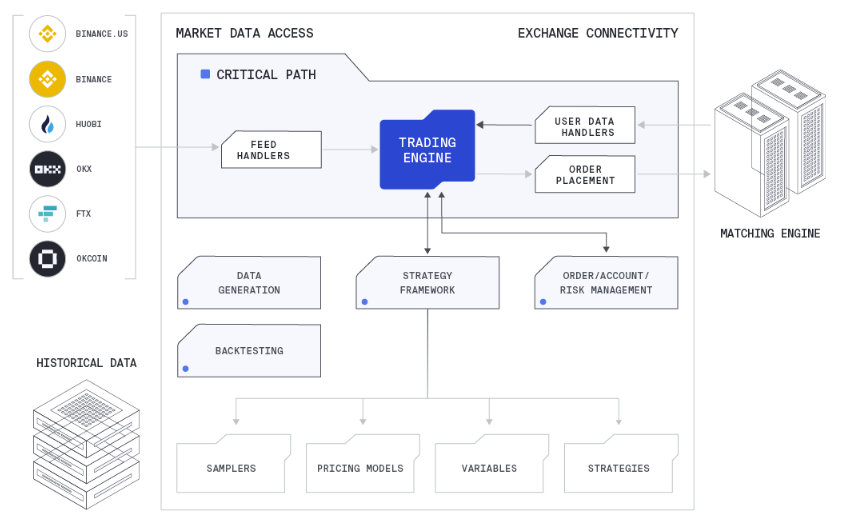

Apifiny Algo introduces a new way to trade cryptocurrencies and their derivatives! It is like an operating system for trading and allows you to trade on many exchanges easily and flexibly. You can pick your preferred way to trade:

-

Configuration-based strategy creation: develop trading strategies like Legos.

-

Generate signals in Python, but execute orders using a high-performance smart executor.

-

Use C++ to speed up your research and trading with little effort. Read more ...

-

Integrate an existing trading system at your preferred level (order placing only, full market access, or just a strategy framework)